In recent years, the emphasis on sustainability and corporate responsibility has surged, leading to a significant evolution in reporting requirements for businesses across the European Union. The Corporate Sustainability Reporting Directive (CSRD), which replaces the non-financial reporting directive (NFRD), marks a pivotal step in this evolution, expanding the scope and depth of sustainability reporting significantly. This blog aims to dissect the nuances of CSRD, focusing on how its data points are reshaping disclosure requirements, and what this means for businesses striving for transparency and accountability.

Understanding the CSRD: What You Need to Know

The CSRD is not just a new set of rules, it’s a comprehensive framework designed to integrate sustainability into the fabric of corporate governance. With an expanded scope that includes all large companies and all companies listed on regulated markets (except micro-enterprises), the directive seeks to bring about a paradigm shift in how businesses report on sustainability issues. The phased implementation, starting from the 2023 financial year, allows businesses time to adapt, but the clock is ticking.

The CSRD requires companies to disclose a broad range of data relating to their environmental, social, and governance practices according to the ESRS technical standards. This includes the consideration of double materiality on how a company both impacts and is impacted by climate change.

Who Does the CSRD Apply to?

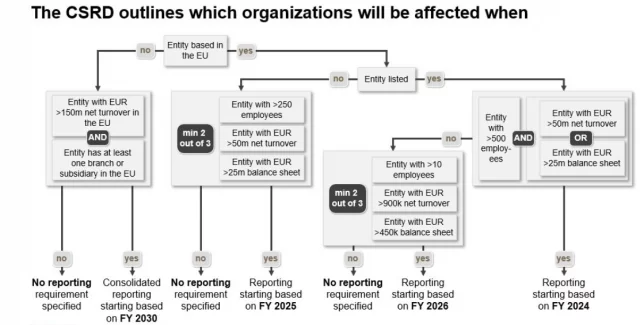

CSRD applies to a broad group of companies that meet, in general, two of the following three conditions:

- €50 million in net turnover.

- €25 million in assets.

- 250 or more employees.

This includes:

- Large, listed corporations, banks, and insurance companies are already subject to the NFRD.

- Other listed EU companies were previously not subject to the NFRD.

- Listed European SMEs (that can report using simplified standards).

- Large private European companies.’

In addition, non-European companies with significant business in the EU (i.e., annual turnover of above €150 million in the EU) will need to comply.

What is the timeline to comply with CSRD?

The rules will start applying between 2024 and 2030. If a company has not yet measured its carbon footprint, it will be important to start getting prepared as soon as possible.

- Reports are due in 2025 for large, listed companies already subject to the NFRD.

- Reports are due in 2026 for large companies not currently subject to the NFRD that meet the requirements stated above.

- Reports are due in 2027 for listed SMEs and all others that meet the requirements stated above, although SMEs have the option to wait until 2030.

The below chart reflects the detailed conditions:

Understanding CSRD Data Points

At the heart of CSRD are the data points that businesses must disclose. These aren’t just any data points; they’re detailed metrics that span environmental, social, and governance (ESG) issues. From greenhouse gas emissions to labour practices and anti-corruption measures, CSRD demands a level of detail and scope unprecedented in non-financial reporting. This new granularity aims to standardize sustainability reporting, making it as rigorous and scrutinized as financial reporting.

Impact on Disclosure Requirements

Under CSRD, companies are required to provide a comprehensive view of their impact on society, the environment, and their governance practices. This includes explaining how sustainability issues affect their business model and strategy, a significant leap from the broad-strokes approach of the NFRD.

Data Quality and Integrity

The directive emphasizes the quality and integrity of sustainability data, akin to financial data’s accuracy and reliability. This shift necessitates robust data collection and management systems, ensuring that the disclosed information withstands scrutiny.

Sector-Specific Impacts

CSRD acknowledges that not all sectors impact sustainability equally. Therefore, it introduces sector-specific reporting standards, acknowledging the diverse nature of sustainability challenges across industries.

Digital Reporting

A key aspect of CSRD is the requirement for digital reporting, making data easily accessible and comparable across businesses. This digital shift aims to foster transparency and facilitate stakeholder analysis.

Challenges for Businesses

Adapting to CSRD is not without its challenges. Businesses face the daunting task of overhauling their data management practices, a process that can be costly and resource-intensive. Small and medium-sized enterprises (SMEs), in particular, may find the financial and operational burden heavy. Moreover, the need for staff training and capacity building cannot be overstated, as understanding and implementing CSRD requirements is a complex endeavour.

Opportunities and Benefits

Despite these challenges, CSRD opens the door to numerous benefits. Enhanced transparency leads to increased trust among stakeholders, including investors, customers, and the public. Additionally, a deeper understanding of sustainability risks and opportunities can lead to better decision-making, potentially unlocking competitive advantages and fostering long-term sustainability.

Preparing for CSRD Compliance

For businesses, the journey toward CSRD compliance begins with a thorough gap analysis to understand where they stand against the new requirements. Investing in technology and data management systems will be crucial, as will engaging with various stakeholders to align expectations and gather insights. Early preparation and a proactive approach to embracing sustainability reporting can turn the challenges of CSRD into strategic opportunities.

Integrating CSRD with Global Sustainability Standards

- Harmonization with International Frameworks: Discuss how CSRD aligns with global sustainability standards and frameworks, such as the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB).

- Impact on Global Reporting Practices: Explore the potential for CSRD to influence sustainability reporting practices worldwide, encouraging a more unified approach to corporate sustainability.

The Role of Technology in CSRD Compliance

- Digital Tools and Platforms: Highlight specific technologies, software, and platforms that can facilitate CSRD data collection, analysis, and reporting.

- Innovations in Sustainability Data Management: Discuss the emergence of new technologies, such as blockchain and AI, in enhancing data integrity and transparency in sustainability reporting.

Stakeholder Engagement and Communication

- Building Stakeholder Trust: Examine the role of transparent and detailed reporting in building trust with investors, customers, employees, and the broader community.

- Effective Communication Strategies: Offer insights into how businesses can effectively communicate their sustainability efforts and achievements to different stakeholder groups.

Regulatory Implications and Compliance Strategies

- Navigating Regulatory Landscapes: Discuss the challenges and strategies for navigating the evolving regulatory landscapes affected by CSRD, including potential overlaps with local regulations.

- Best Practices for CSRD Compliance: Share insights and best practices from industry leaders and early adopters of CSRD compliance, including how to leverage CSRD for strategic advantage.

Future Trends in Sustainability Reporting

- Predictions for the Evolution of CSRD: Offer insights into how CSRD requirements might evolve and what future iterations might look like.

- The Next Frontier in Corporate Sustainability: Discuss upcoming trends in sustainability and corporate responsibility, and how businesses can prepare for future expectations in reporting and performance.

Conclusion

The introduction of the CSRD marks a significant milestone in corporate sustainability reporting, with its emphasis on detailed data points and comprehensive disclosure requirements. While the path to compliance may be challenging, the directive offers businesses a unique opportunity to lead with transparency, enhance their sustainability performance, and build trust with stakeholders. As we move towards a more sustainable future, the CSRD stands as a testament to the pivotal role of transparency and accountability in driving positive change.