As we step into a stage in the financial reporting landscape where transparency and consistency become more challenging, IFRS 18 emerges as an accounting standard that will revolutionize not only how performance is reported, but also how performance is explained. What is interesting about this specific webinar is that it did not concentrate on the actual language of the IFRS 18 but rather on problems with its implementation.

What the New Standard Means for Financial Reporting

The implications of IFRS 18 go beyond technical requirements for the presentation of the financial information of an entity. The standard redefines the way that a company presents financial statements and explains performance while supporting its strategic perspective.

Strategic Implications of IFRS 18

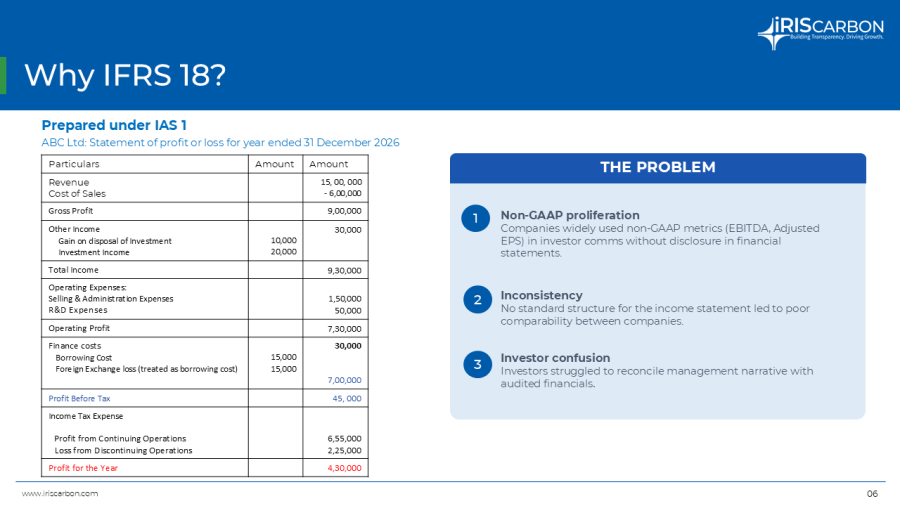

For many years, companies had the significant freedom of preparing their profit or loss and other performance measures. This was one of the reasons why financial statements were hard to compare between entities and different periods.

IFRS 18 aims to reduce that inconsistency by introducing a more structured approach to presentation and disclosure. The result is a reporting model that gives users a better view of operating performance, financing impacts, and management-defined metrics.

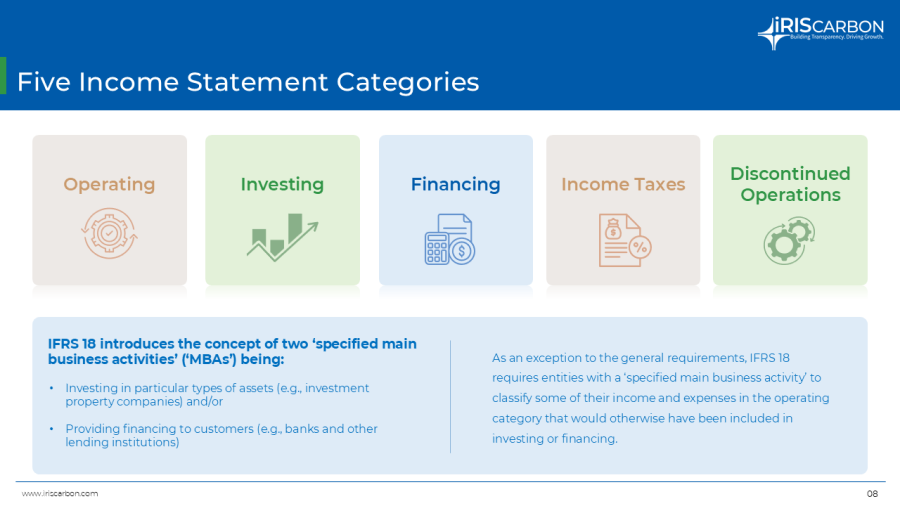

The Core Changes: 5 Categories and 2 New Subtotals

As per IFRS 18, there will be a restructuring of the profit/loss statement. Unlike before where companies were allowed to determine how income items and expenses would appear, the new standard requires all income items and expenses to be arranged within one of five categories: Operating, Investing, Financing, Income Taxes, and Discontinued Operations.

Two Mandatory Subtotals

In order to make sure that there will be uniformity across the world and to help the investor forecast, there are two mandatory subtotals to be found in the income statement, namely Operating Profit and Profit or Loss Before Financing and Income Tax.

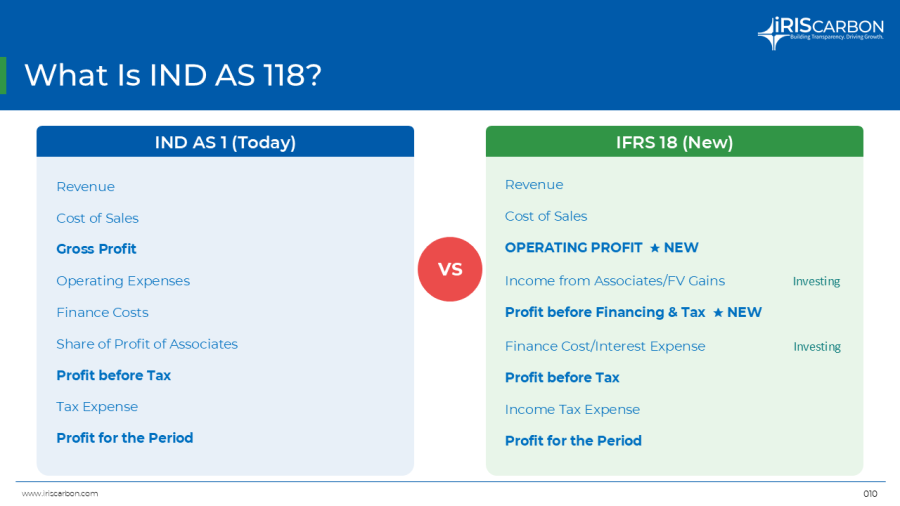

The structural difference between the old standard (IAS 1) and the new mandatory flow under IFRS 18 was clearly contrasted during the session

IFRS 18 decreases the level of freedom that can be applied while preparing the income statement in order to make the companies easy to compare all over the world. Operating profit becomes a standard opening point for presenting business performance, the investing income (such as associates’ profit) is removed to show the income not related to the company’s core operations and there is introduced a new subtotal, Profit before Financing & Tax, in order to present results before interests and taxes.

Overall, it creates a cleaner, more consistent structure for analysing a company’s performance.

Performance Measures Now Need More Discipline

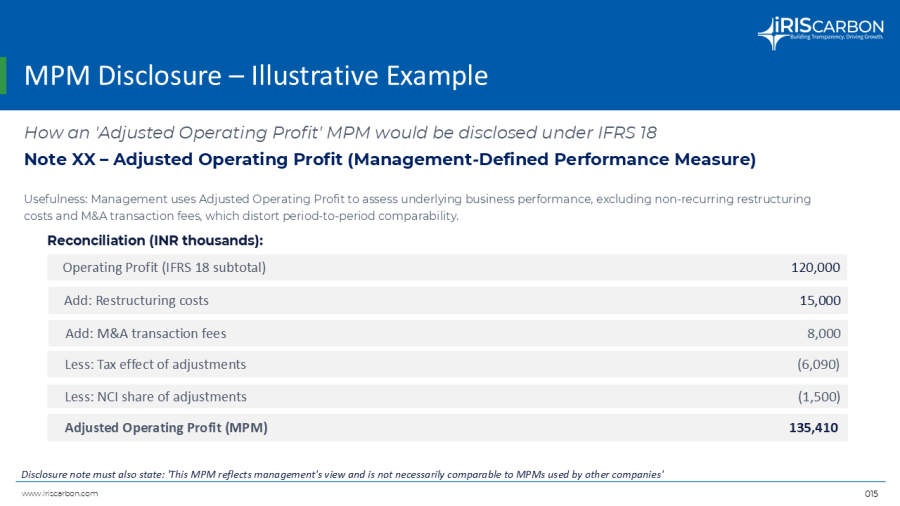

A major focus of IFRS 18 is management-defined performance measures. These are the subtotals which are used by companies for communication purposes, and which reflect the way the management sees its performance.

If you use some other subtotal provided by your management team, then according to IFRS 18, you should include such measure in a special note within the audited financial statements. This note should include a description of the measure, its calculation method, its reconciliation with the closest comparable IFRS subtotal and the tax/NCI effect.

Here is an illustrative example of the way that “Adjusted Operating Profit” MPM needs to be formally reconciled under the new rules:

Operational Obstacles: Key Challenges

As demonstrated in the webinar, switching to IFRS 18 is a cross-functional challenge much bigger than just a simple accounting switch. Specifically, the webinar identified the following key challenges that must be overcome:

What To Do Next

A practical approach to the challenge would involve starting from the beginning. Companies need to reconcile their current reporting system to the new one outlined in IFRS 18, determine which measures might be considered as management-defined performance measures, and examine if the company’s systems will allow proper disclosures.

Here are five important points you should keep in mind:

- It Is a Disclosure Problem, Not an Accounting Solution: The approach shifts attention from accounting tasks to financial reporting strategy, changing the way the story of corporations is told.

- Income Statement Gets a New, Mandatory Flow: Disallows management’s freedom of choice by introducing the five inflexible categories and two necessary subtotals in the P&L.

- MPMs Under Audit Scope Now: Adopts metrics used in investor presentations right into the audited financial statements, where a single footnote must cover all qualified MPMs.

- No More “Other Expenses”: Stops the practice of combining inconsistent costs together, obliging companies to aggregate costs according to their characteristics, in addition to five required nature-of-expense disclosures.

- Spreadsheets Will No Longer Work: Demands profound reconfiguration of data flows within the ERP system along with aligning KPIs and compensation metrics.

Dive Deeper into the Framework

Adapting your disclosure strategy to match the strict mechanics of IFRS 18 requires careful planning, rigorous data mapping, and updated digital disclosure workflows.

The full webinar dives deeper into a step-by-step comparative look at statements under IAS 1 vs. IFRS 18 and provides an illustrative example of a compliant MPM reconciliation note.

The webinar is highly recommended viewing for those whose job is related to financial reporting, ERP changes, and governance.

Download the webinar deck here.