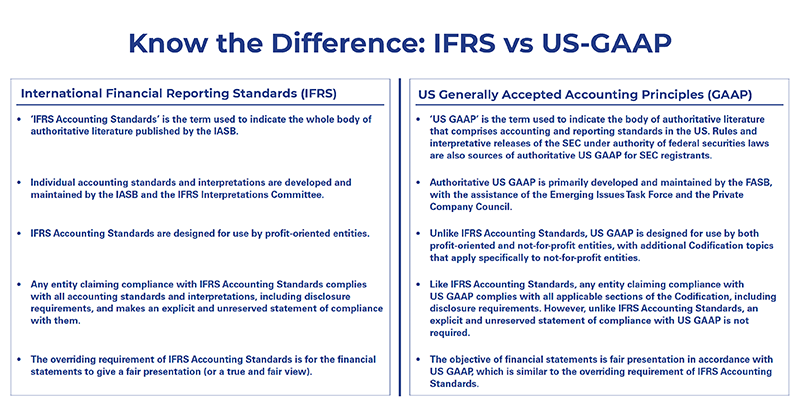

Foreign Private Issuers (FPI) operate in a unique accounting universe. International Financial Reporting Standards (IFRS) offer the conceptual freedom to interpret principles in a way that suits the business context. The United States Securities and Exchange Commission (SEC), however, expects the rigorous clarity of rule-based reporting. Form 20-F is the point where these two philosophies meet and sometimes collide.

Most finance leaders understand the technical gaps between IFRS and US GAAP, but the real burden lies in reconciling the two. The SEC estimates that preparing a single Form 20-F takes about 660 hours, which reflects how much time FPIs spend translating IFRS positions into US GAAP-compliant disclosures.

The complexity grows because FPIs cannot treat the 20-F as a once-a-year task. Even if they file only annually, they still maintain internal quarterly reporting under IFRS while preparing for a filing that must meet US GAAP expectations. This year-round reconciliation effort is why the 20-F consistently demands more time, attention, and resources than most FPIs anticipate.

Where IFRS and US GAAP Differences Create Real-World Reporting Bottlenecks

Although IFRS and US GAAP differ in technical detail, it is the operational ripple effects that consume time and heighten reporting risk.

1. Judgment versus Documentation Creates Excessive Support Requirements

IFRS encourages interpretation, and while this flexibility is helpful for economic storytelling, it creates a parallel responsibility to document every judgment when preparing US GAAP-compatible disclosures for the SEC. As assumptions are revisited and updated, reporting teams are forced to maintain a sprawling collection of files, supporting schedules and commentary versions that evolve continuously throughout the reporting cycle.

2. One Change Can Cascade Across an Entire Reporting Package

An update in an IFRS estimate affects the GAAP reconciliation and triggers changes across the financial statements, notes, MD&A narrative, operational KPIs, and risk factors. When reporting workflows rely on spreadsheets and email threads, this cascade becomes slow, unpredictable and difficult to control, leading to last-minute revisions that strain both teams and auditors.

3. SEC Expectations Require Perfect Alignment of Numbers and Narrative

The SEC has consistently increased expectations around transparency, consistency, and Inline XBRL (iXBRL) accuracy. FPIs are expected to reconcile not only their financial statements but also the story around those numbers. This means every sentence in the MD&A must align with the financial statements with absolute precision, something that spreadsheet-era processes cannot govern effectively.

Source: KPMG

The Missing Impact: Disconnected IFRS and GAAP Processes Hinder Decision-Making

Most discussions on IFRS and GAAP focus on accounting. The real cost, however, is strategic.

44 hours every week are wasted on manual finance tasks, slowing the reporting cycle. When reconciliations require weeks of manual work, organizations lose precious time that could have been spent on forward-looking analysis. Controllers spend their judgment hours reconciling spreadsheets instead of strengthening internal controls. CFOs receive financial visibility too late to influence strategic decisions. Business leaders wait for insights that arrive only after the close, which means decisions are made with partial or outdated information.

Modern enterprises cannot afford this pace, especially when the reporting landscape is moving toward real-time accuracy and continuous assurance. According to McKinsey, AI has the potential to automate 60-70% of work activities, and this shift fundamentally changes how finance teams allocate their time. Instead of spending weeks validating reconciliations, they can focus on the interpretation, scenario planning, and risk assessment that actually influence growth and resilience.

This is where a data-centric disclosure management environment becomes transformative

Rethink SEC 20-F Filing with Automated Disclosure Management

Broadly speaking, disclosure management platforms enable finance teams to standardize disparate financial data coming from various data sources within an organization. This helps prevent incorrect data from entering the disclosures, reduces time spent on oversight, and helps build reporting confidence.

In SEC 20-F reporting where issuers work with different accounting standards, a disclosure management platform helps converge numbers and narrative into US-GAAP standards to meet compliance requirements. Its connected environment enables reporting teams to visualise complex data through a single administrative pane, making it easier to draw insights that expedite decision making.

The following are some of the instances where disclosure management helps FPIs streamline 20-F filings.

1. IFRS and GAAP Data Come Together in a Unified Reporting Backbone

A modern disclosure management platform allows every financial statement line, footnote input, KPI and narrative section to pull from centrally governed data. Once a value is updated at the source, it updates everywhere it appears. This removes duplicated work, repetitive checks, and the risk of inconsistent versions circulating across teams.

2. Every Change Is Fully Traceable with Strong Governance

Audit trails, automated validations, and real-time consistency checks ensure that every change is captured, and every mismatch is flagged instantly. This gives controllers and auditors visibility across the entire process and dramatically reduces the end-of-cycle pressure that typically surrounds the 20-F.

3. AI Simplifies IFRS to GAAP Reconciliations

AI helps identify accounting differences, evaluate their impact across financial statements, and assist in drafting the reconciliation notes. It also compares current period data with previous filings to detect unusual movements and potential inconsistencies, allowing teams to review insights rather than hunt for errors.

4. iXBRL Becomes a Natural Output

When data is structured, tagged and validated throughout the reporting cycle, iXBRL accuracy improves significantly. AI-supported tagging and automated rule-based checks ensure that the 20-F is consistently aligned, both numerically and narratively.

Build Pace, Proficiency and Trust into Your 20-F Filings

Once FPIs reduce the friction of reconciling IFRS and US GAAP, the advantages reach far beyond SEC compliance.

Close cycles shorten. Rework drops dramatically. Reporting quality improves. Most importantly, decision-makers finally get timely insight into how differing accounting treatments influence performance, valuation and investor communication. This gives the CFO and leadership team a more confident foundation for strategy and risk decisions, especially in volatile market conditions.

What This Means for Forward-Looking Foreign Private Issuers

FPIs do not need more spreadsheet templates or more review layers. They need an integrated reporting model that treats IFRS and GAAP differences as connected data transformations rather than manual rework. A modern disclosure management platform provides exactly this environment through:

- Centralized data linking across IFRS & GAAP.

- AI-driven reconciliations and variance insights.

- Continuous audit readiness with full control visibility.

- iXBRL accuracy baked directly into the workflow.

- Collaborative drafting with strong governance.

- A single version of truth across every disclosure.

The accounting differences between IFRS and US GAAP will always exist. The operational burden does not have to. FPIs that modernize their disclosure processes today will gain a competitive advantage in accuracy, speed and strategic decision-making for years to come.