The digital or machine-readable format has revolutionized the way business information is consumed. Financial reports in the eXtensible Business Reporting Language (XBRL) are widely produced and disseminated, bringing benefits such as transparency and comparability of information to all stakeholders. And now, the next big thing in digital reporting is Environmental, Social, and Governance (ESG) disclosures.

In recent blog posts, we have explored various facets of ESG reporting such as its significance, the available sustainability standards, and the need for digital disclosure. In this blog, we will take a look at efforts by the European Financial Reporting Advisory Group (EFRAG) to draft a set of sustainability standards for companies in the EU. Those standards would be used for reporting in accordance with the Corporate Sustainability Reporting Directive (CSRD) from January 2024 onwards.

The EFRAG recently released a draft taxonomy for digital sustainability reporting. The [draft] Standard covers disclosure requirements related to “Climate change mitigation”, “Climate change adaptation” and “Energy”.

The contents of the draft EFRAG taxonomy shall be read in conjunction respectively with ESRS 1 General Principles and ESRS 2 General, Strategy, Governance and Materiality Assessment. ESRS stands for European Sustainability Reporting Standards.

The taxonomy focuses on the (GHGs) Green House Gas emissions, which are further divided as emissions by segment and by country.

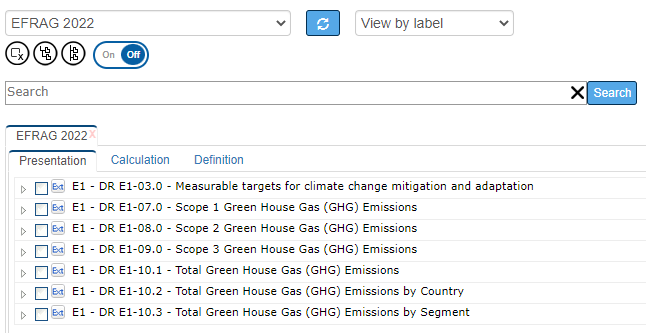

Here’s a Snapshot of the EFRAG Draft Taxonomy.

The draft EFRAG taxonomy includes the following:

1. Measurable Targets for Climate Change Mitigation and Adaptation

Text Block concepts:

The taxonomy elaborates on Measurable targets for climate change mitigation and adaptation by targeting the ‘Baseline year’ and the Climate-related targets that have been adopted.

This requires issuers to disclose ‘Text Block’ information on the progress of measures on climate change, and if the standards have not been adopted, the reasons for such failure.

This ‘Extended Linkrole’ also covers the information to be tagged for the measures, such as when and how they will be adopted.

The Greenhouse emission reduction targets, which are crucial, will have to be disclosed along with scientific explanations.

Fact Value Concepts:

The Taxonomy has laid a structure with ‘Target Values of Greenhouse Gas (GHG) emission’ and ‘Contribution of decarbonization’ root level abstract.

This mainly captures the fact-value information of GHG emissions, descriptions of lever assumptions, and GHG emission reduction classified on the basis of ‘Scope of Reporting; (Axis) and the ‘Lever Category’ (Axis).

2. Scope of GHG Emissions

The scope of GHG emissions requires information on the Carbon Dioxide equivalent, the share of Target or Base year, and the Annual Target or Base Year by Scope I entities only.

3. Total GHG Emission

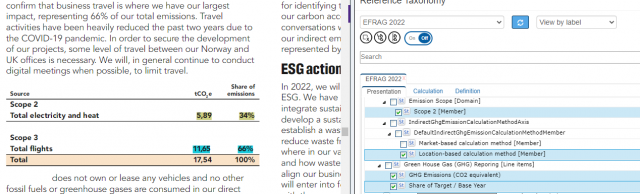

The total GHG Emission disclosure requires the issuer to disclose the information Country-wise and/or Segment-wise for two broad factors:

- GHG Emissions (CO2 equivalent)

- Share of Target/Base Year

The taxonomy structure focuses on the Scope and GHG Emissions, whether direct or indirect. Below is an example of value tagging using the draft EFRAG Taxonomy.

We hope you find this brief snapshot of the EFRAG taxonomy. We are awaiting more updates on the same. Follow our blog for further information about sustainability reporting under the CSRD regime.