Text block tagging is a major addition to ESEF filing requirements for the upcoming reporting cycle. Phase II of the mandate is applicable from January 1, 2022, i.e. for annual reports ending 31st December 2022. As per phase II of the mandate, every note forming a part of Financial Statements will be required to be block tagged with XBRL tags.

What is Block Tagging?

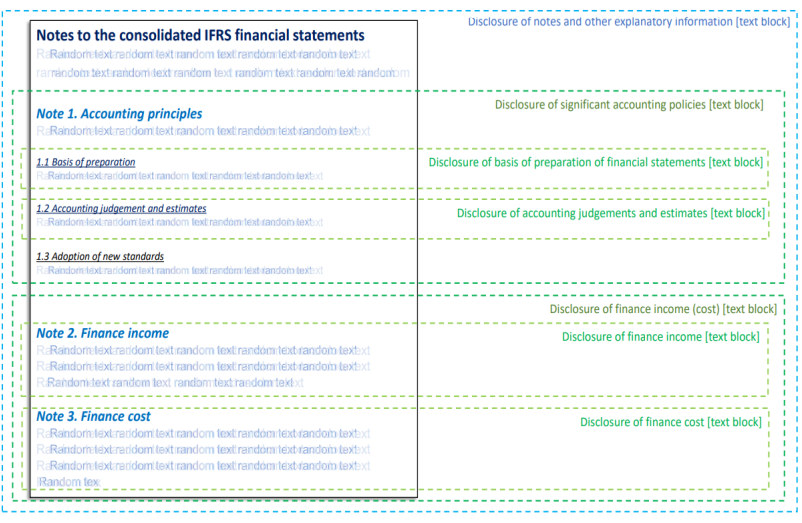

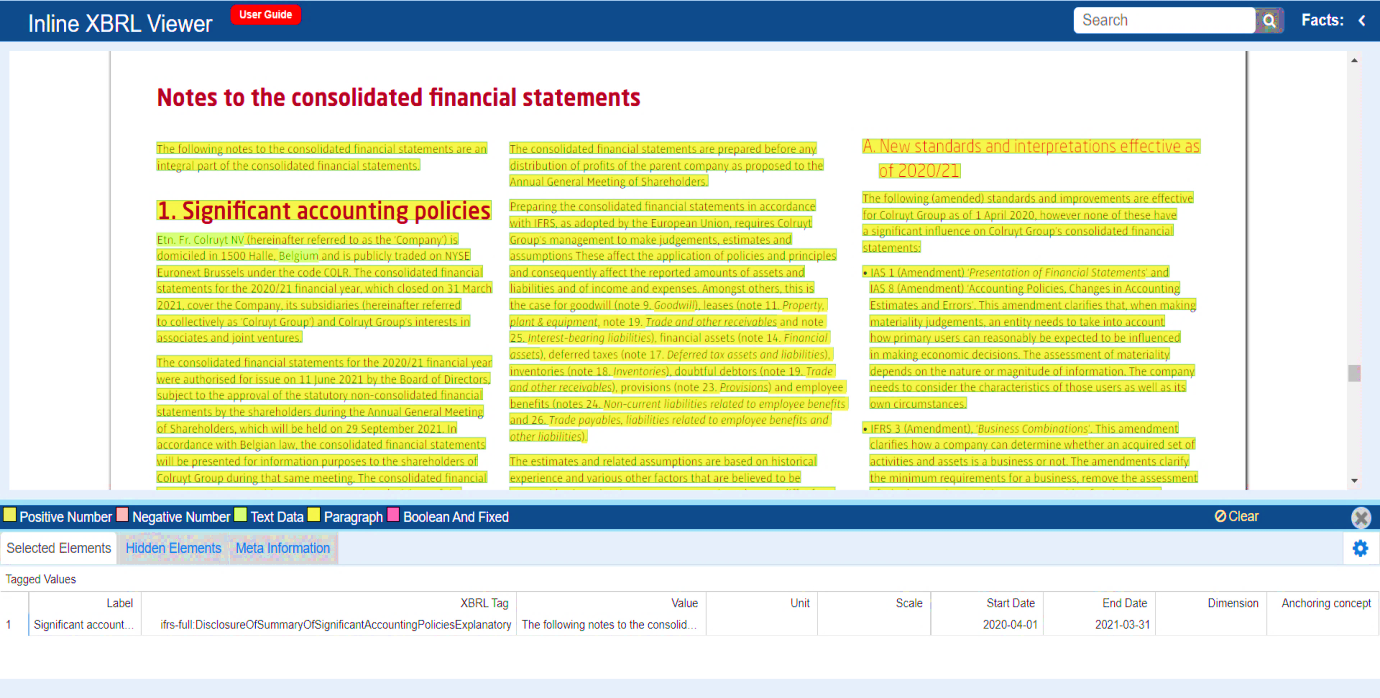

In the case of the notes to Financial Statements, each note will be treated as a single fact and will be tagged with a single “TextBlockItemType” element. A text block tag may include text, numeric values, tables, and other data contained in a single note.

Guidance: What does the ESEF reporting manual say about Block tagging? The manual says every note is recommended to have an XBRL tag associated with it. Refer to Guidance 1.3.3 on Tagging elements (Tables 1 and 2) of Annex II in the manual.

What does the ESEF Reporting Manual say about Block Tagging?

The European Securities And Market Authority (ESMA) released an updated ESEF reporting manual on August 5, 2022, which was much awaited after the EU conference held in Paris in July 2022. In annual reports where the reporting period starts on 1 January 2022, issuers need to block tag policies and notes with XBRL tags, along with the primary financial statements.

Tagging of the Notes to Accounts

A few elements in the ESEF Taxonomy defined as “TextBlockItemType” are expected to be used for marking up (following the block tagging approach) larger pieces of information contained in IFRS consolidated financial statements such as explanatory notes and accounting policies.

ESMA is of the opinion that issuers shall, at a minimum, mark up the information contained in IFRS consolidated financial statements (including headers/titles) with TextBlockItemType elements. In the case of disclosures corresponding to more than one element of different granularity (with wider and narrow elements), preparers should use each of them and multi-tag the information to the extent that corresponds with the underlying accounting meaning of the information.

The 2021 ESEF Taxonomy contains various ‘TextBlockItemType’ elements. The TextBlockItemType elements usually start with the prefix ‘DisclosureOf…’. These elements are to be used to tag the narratives in the notes to financial Statements. The narratives may include information in tabular format; they may also include headers or numbers and other larger pieces of information.

ESMA recommends that the issuers shall at least mark up the information contained in IFRS consolidated financial statements (including headers/titles) with the TextBlockItemType elements. There are in general 230 elements that can be tagged starting from the 2022 annual report. Of these 230 elements, around 132 start with the prefix ‘Disclosure of…’ and around 98 start with the prefix ‘Disclosure of accounting policy of…’ and around 32 text block elements are categorized under other residuary categories.

Example of multi-tagging the notes to the consolidated IFRS financial statements with the elements of Annex II

The Granularity of Block Tagging

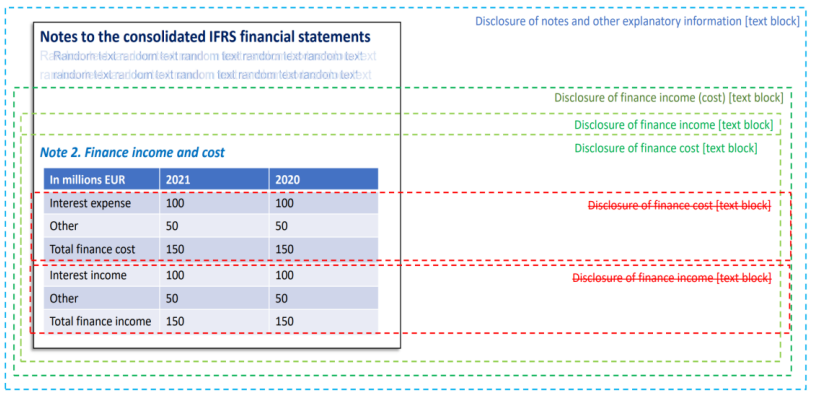

In certain cases, the block tagging of notes contains tables (different columns/rows) and different tags within the taxonomy. ESMA has said that issuers are not required to apply “TextBlockItemType” elements on selected rows or columns of such tables. Instead, they shall apply corresponding elements to the entire table. In case the disclosure includes numbers or values in tabular format, then such numeric data is not required to be tagged with ‘Monetary Concept’ XBRL tags.

Example of the granularity to tag a table in the notes to the consolidated IFRS financial statements

Other Considerations for Block Tagging

There is no obligation to create an extension to tag the Notes to financial statements if the disclosure does not correspond to any of the elements in the taxonomy. But ESMA encourages issuers to create an extension block tag since this information is useful to the end users i.e. investors and analysts.

Also, there is no obligation to anchor extensions in the Notes to financial statements, but again ESMA encourages the anchoring of extensions to maintain consistency across reporting periods to the maximum possible extent.

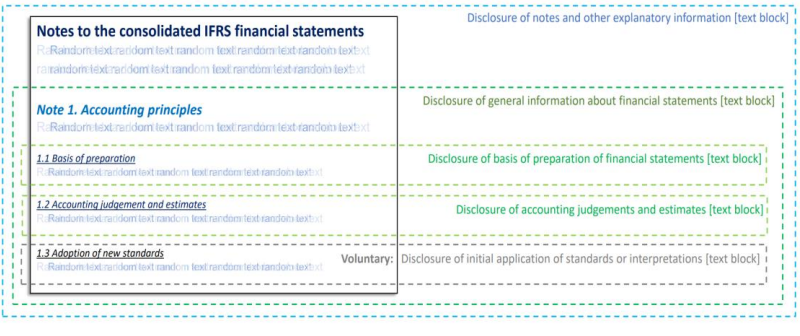

Example of multi-tagging the notes to the consolidated IFRS financial statements when including voluntary elements.

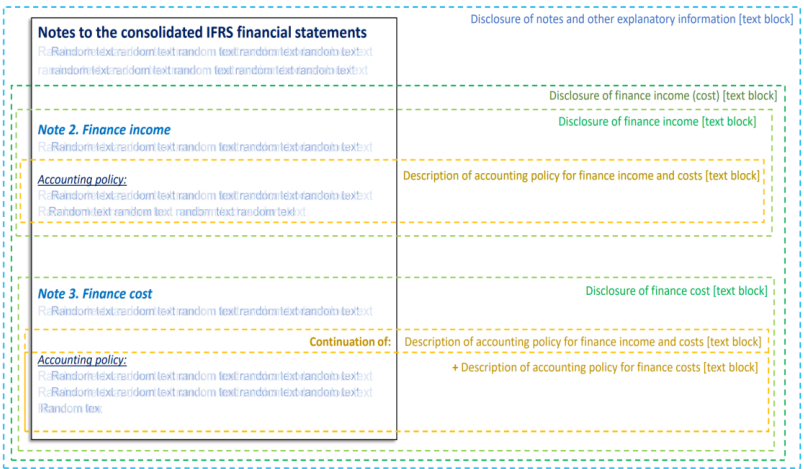

In instances where multiple pieces of text corresponding to one block tag are disclosed in different sections of the notes, issuers should tag such disclosures with one block tag by using Inline XBRL constructs which allow the concatenation (or exclusion) of text content within a document.

For Example…

IRIS CARBON® supports both Phase 1 and Phase 2 tagging requirements of the ESEF mandate. Here’s how to block tagging looks on the IRIS CARBON® platform.

ESEF Phase II Early Birds

A few companies IRIS CARBON® is working with proactively adopted Phase 2 ESEF tagging requirements with their 2021 annual reports ready themselves for mandatory block tagging requirements. Given below are iXBRL previewer links from the IRIS CARBON® platform of two companies that voluntarily adopted block tagging. An iXBRL previewer link can be published on a company website for the benefit of investors and analysts.

Inline XBRL Viewer (iriscarbon.com)

Inline XBRL Viewer (iriscarbon.com)

With IRIS CARBON® you can either outsource ESEF tagging or opt to do it in-house using our solution. Either way, you partner with a software vendor who has facilitated over 250 ESEF filings across the European Union.