There’s an uncomfortable truth sitting at the center of financed emissions reporting today. Most banks are already disclosing financed emissions. Most of those numbers are still largely estimated. And everyone in the room knows this won’t hold up for long.

That tension set the tone for our recent webinar, “Financed Emissions in Practice: What Banks Do When the Data Isn’t There.” Instead of theory, the discussion focused on what actually happens inside banks trying to build credible, audit-ready financed emissions frameworks.

As Farzad Wadia, Director – ESG Solutions at IRIS CARBON®, put it early on:

“Most banks today are disclosing financed emissions with a number that’s largely an estimate… everyone knows in the industry that this really won’t last.”

So, what are banks doing in the meantime?

The Reality Check: Financed Emissions Are Mostly Estimated

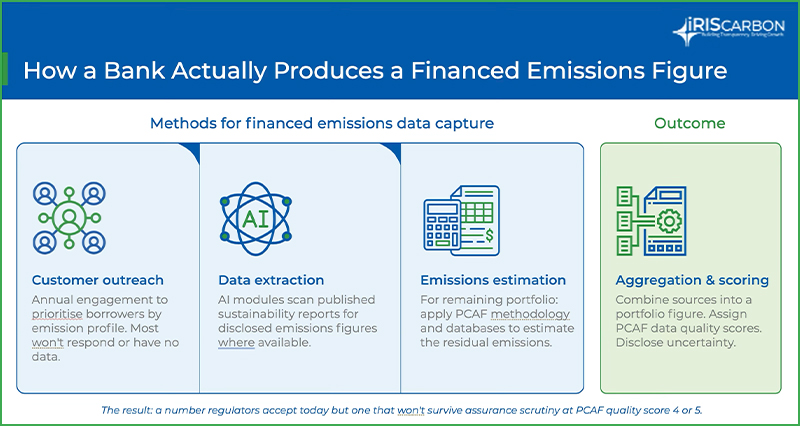

The first takeaway is hard to ignore: financed emissions dominate a bank’s climate footprint, yet the underlying data is still fragile.

“95% of a bank’s carbon footprint flows through its loan book… not its offices or operations.” But here’s the problem. That footprint depends on borrower data that often doesn’t exist.

So, banks improvise:

- They ask customers for emissions data (most don’t have it).

- They extract what they can from public reports.

- And they estimate the rest using PCAF methodologies.

The result? A number that works for disclosure today but may not survive assurance tomorrow.

“You’re essentially building a number from averages, not measurements.”

This gap between what’s reported and what’s defensible is closing fast, especially as regulations tighten.

The Shift That Changes Everything: From Compliance to Value

One of the most practical insights from the session was how banks are reframing from the conversation.

Instead of asking:

“Share your emissions data so we can report.”

They’re shifting to:

“This data helps you understand your costs, risks, and efficiency.”

Roxana explained how this changes the dynamic:

“It’s not about transferring data without understanding it. It’s about helping customers see what that data means for their own business.”

When customers see value like cost savings, efficiency gains, risk visibility, they’re far more willing to engage.

Beyond Compliance: How Banks Are Rethinking Financed Emissions and Where It Falls Short

Banks are moving beyond disclosure to make financed emissions reporting more meaningful, for themselves and their customers. But while the approach is evolving, the underlying challenges around data, engagement, and scale haven’t gone away. Here’s where progress meets friction:

1) Why Customer Participation Is the Real Challenge

If there’s one part of the webinar that stood out, it’s this: financed emissions is not just a data problem. It’s a customer problem.

Roxana Barbato, ESG & Sustainability Director at Raiffeisen Bank Romania, brought a ground-level perspective:

“It’s not enough for regulators or banks to act. You need the customer at the table… because in the end, it’s everybody’s target.”

But getting customers to share data isn’t straightforward.

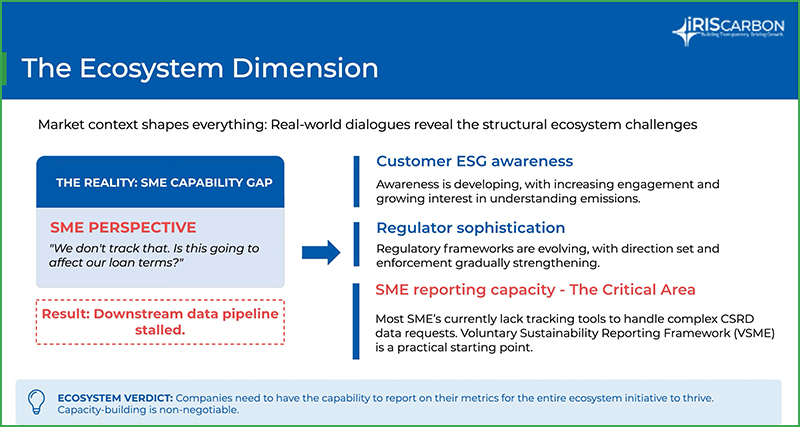

2) Where the Data Ecosystem Falls Short

Even with better conversations, there’s a structural issue: the ecosystem isn’t ready.

- SMEs lack tools and capacity.

- Reporting awareness is still developing.

- Regulatory pressure isn’t evenly distributed.

As a result, the data pipeline breaks downstream.

“The reality is SMEs don’t track this data… because they’ve never had to.”

This is where frameworks like VSME (Voluntary Sustainability Reporting for SMEs) come in. They offer a simplified way for smaller companies to start reporting without heavy investment.

And for banks, that’s a critical unlock:

- Better data quality.

- More consistent inputs.

- Stronger customer relationships.

3) What Technology Can and Cannot Fix

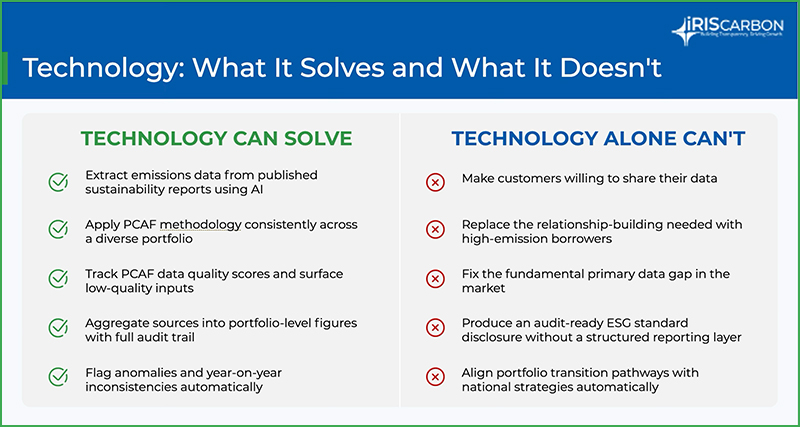

There’s a lot of noise around AI and ESG tech. The webinar cut through that quickly.

Yes, technology can:

- Extract emissions data from reports.

- Apply PCAF methodology consistently.

- Track data quality and audit trails.

- Aggregate portfolio-level insights.

But it cannot:

- Make customers willing to share data.

- Replace relationship-building.

- Create primary data where none exists.

“Technology solves parts of the problem. But the hardest parts are still human.”

4) Why Excel-Based Financed Emissions Reporting Won’t Scale

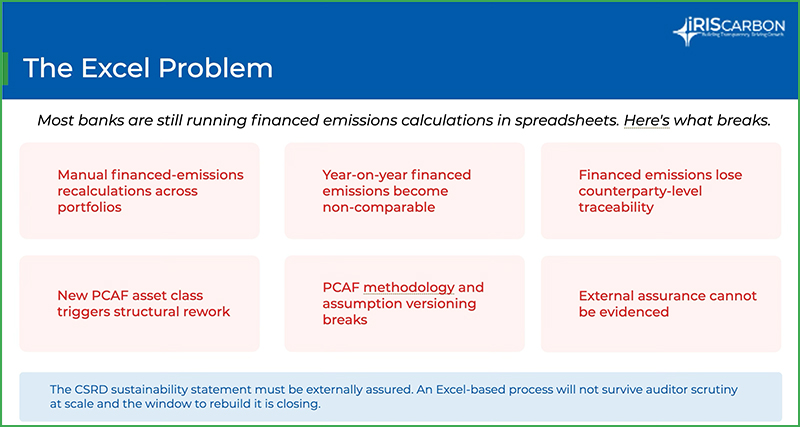

One of the more relatable moments in the session was the discussion on spreadsheets.

Most banks still run financed emissions calculations in Excel.

And it works… until it doesn’t.

- No audit trail

- No version control

- No consistency across periods

- Difficult to scale

“An Excel-based process will not survive auditor scrutiny at scale.”

As assurance requirements increase, this becomes a breaking point—not just an inefficiency.

What Actually Works: A Bank’s Real-World Approach

Roxana shared how Raiffeisen Bank approached this in practice, and the takeaway is clear: real-world implementation shows that improving financed emissions data is a gradual process.

Raiffeisen Bank’s approach includes:

- Starting with PCAF-aligned estimates.

- Gradually integrating primary data.

- Using AI for disclosure extraction.

- Engaging customers through ongoing dialogue.

But even then, challenges remained:

“We saw a lot of fluctuations… depending on how the portfolio evolved.”

Which leads to an important insight: financed emissions isn’t static. It moves with your portfolio, your customers, and your strategy.

So, banks are now:

- Segmenting customers based on emissions profiles.

- Aligning engagement strategies accordingly.

- Linking financing to sustainability performance.

Why Financed Emissions Reporting Matters for Sustainable Finance

Financed emissions are central to sustainable finance reporting and the transition to a low-carbon economy.

“If we want a net-zero future, capital allocation is key… and financed emissions sit at the heartbeat of it.”

Banks are building these frameworks in real time, balancing incomplete data, evolving standards, and increasing regulatory expectations.

Want the Full Picture?

This blog only scratches the surface of what was discussed. The full webinar dives deeper into:

- How banks defend estimated numbers to auditors.

- What real customer conversations sound like.

- Where technology delivers ROI (and where it doesn’t).

- A detailed case study from Raiffeisen Bank.

If you’re working on financed emissions, ESG reporting, or sustainable finance strategy, it’s worth watching end-to-end.

Watch the full webinar recording here.