How energy companies are adapting to Order 860/859 compliance, and what finance leaders now expect from modern FERC XBRL reporting software.

If you’ve been filing FERC regulatory forms for any length of time, you remember what life looked like before Order No. 859.

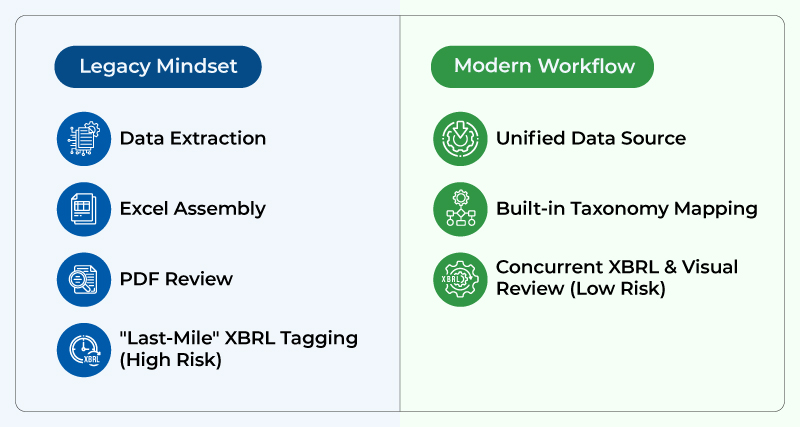

PDF submissions. Spreadsheets emailed back and forth. Manual data entry that consumed significant time during every reporting cycle. Then FERC flipped the switch, and everyone had to figure out XBRL in a hurry.

That was 2019 when the Commission issued Order No. 859, formalizing the mandate for XBRL-based digital filing. Full implementation rolled out in November 2021 across Forms 1, 1-F, 2, 2-A, 3-Q, 6, 6-Q, 60, and 714.

Four years on, the dust has mostly settled, but “mostly” is doing a lot of work in that sentence. The questions CFOs, Controllers, and FERC compliance analysts are now asking aren’t whether to adopt FERC XBRL reporting software. It’s whether their current setup is actually built for what FERC has become: a living, annually-updated taxonomy standard that only keeps getting more complex.

How FERC Orders 860 And 859 Changed Energy Reporting Requirements

On paper, the transition to structured reporting appeared straightforward: map disclosures to taxonomy, validate, and submit filings. In practice, Orders 860 and 859 introduced a deeper expectation, data that is machine-readable, comparable, and internally reconciled across reporting periods.

This distinction has materially changed what finance teams are responsible for.

Today, teams must ensure:

- Consistency between FERC filings and internal financial statements.

- Traceable XBRL tagging logic across reporting cycles.

- Reduced manual intervention in instance document creation.

- Audit-ready documentation of tagging decisions.

FERC reporting is no longer a formatting requirement. It is a controlled data process.

And that shift has exposed limitations in how many organizations originally implemented their FERC XBRL reporting software.

How FERC XBRL Reporting Software Is Typically Used Today

Despite years of adoption, many energy companies still rely on fragmented reporting environments that include Excel-based preparation, manual tagging layers, and separate validation tools.

This structure creates predictable operational bottlenecks:

| Manual Dependency In FERC XBRL Tagging Processes | Version Control Issues Across FERC Reporting Cycles | Late-Stage Validation Increases Filing Risk | Limited Audit Traceability In FERC XBRL Reporting Software Setups |

When these bottlenecks collide during a compressed closing window, compliance moves from a structured routine to a fire drill. These frictions have driven the five core lessons the industry has learned since the transition.

Five Lessons Learned From the FERC Digital Transition

After multiple reporting cycles, several lessons consistently appear across energy companies, utilities, and pipeline operators.

These lessons are shaping how finance leaders approach compliance investments today.

Lesson 1: The Fallacy of the “Last-Mile” Tagging Mindset

The idea of completing a report first and applying XBRL tags later may appear efficient on the surface.

In reality, it often creates bottlenecks.

Issues discovered during tagging frequently require teams to revisit schedules, recalculate disclosures, or revise supporting documentation. What initially appears to save time often results in more rework during the most time-sensitive part of the filing process.

Organizations with mature reporting processes increasingly integrate tagging and validation much earlier in the reporting cycle.

Lesson 2: Operational Capacity Beats Technical Complexity

During the early days of the transition, vendor marketing focused heavily on technical complexity. However, practical application has shifted the corporate focus away from technical jargon and toward internal operational capacity and platform stability.

When a lean corporate reporting team is managing multiple entities under a tight deadline, the primary challenge isn’t complex taxonomy design, it’s bandwidth.

During peak filing windows for quarterly Form 3-Q or annual Form 1 and Form 2 submissions, the focus must remain entirely on control, predictability, and execution speed

Early discussions about FERC XBRL reporting focused heavily on taxonomy structures and technical implementation.

Today, most finance leaders view the challenge differently.

The real question is whether reporting teams can manage multiple filings, review cycles, and regulatory deadlines without creating operational strain.

The most successful implementations are often not the most technically sophisticated. They are the ones that simplify execution and reduce dependency on manual processes.

Lesson 3: Disconnected Reporting Systems Create Regulatory Risk

As reporting becomes increasingly data-driven, inconsistencies across systems become more visible.

A number reported in a financial filing, operational disclosure, or affiliate reporting submission should tell the same story.

When reporting systems are disconnected, organizations spend more time reconciling information and responding to questions that could have been avoided altogether.

Lesson 4: Preparing for XBRL-CSV Cannot Wait Until The Deadline

The industry’s reporting future is moving beyond traditional filing structures.

The introduction of XBRL-CSV requirements for Electric Quarterly Reports (EQRs) signals a shift toward high-volume, transaction-level reporting.

Organizations that continue to rely on manual workflows will find scaling increasingly difficult as reporting volumes grow.

For finance leaders, the conversation is no longer whether automation is necessary. The conversation is whether current reporting infrastructure is capable of supporting future reporting requirements.

Lesson 5: The Biggest ROI Comes From Control, Not Compliance

Perhaps the most important lesson is that the value of modern reporting platforms extends well beyond regulatory compliance.

Organizations that invest in robust reporting infrastructure often see benefits in areas such as:

- Reduced audit effort

- Stronger internal controls

- Improved reporting consistency

- Faster review cycles

- Better cross-functional collaboration

The return on investment is rarely limited to filing efficiency alone, it yields measurable returns across three pillars:

| Strategic Pillar | The Legacy Drag | Modern Platform ROI |

| Audit & Advisory Costs | High billable hours spent manually tying out files and verifying XBRL instance integrity. | Drastic reduction in external audit verification hours due to native, system-generated audit trails. |

| Enterprise Strategy | Fragmented tools for SEC (10-K), FERC, and EPA reporting, creating data discrepancies. | A single source of truth where a data point is changed once and flows identically to all disclosures. |

| Human Capital | High-performing financial analysts burning out on manual data entry and formatting bugs. | Automation of low-value tasks, allowing strategic talent to focus on analytical review and operational velocity. |

What Finance Leaders Should Look For In FERC XBRL Reporting Software In 2026

The market for FERC XBRL reporting software has matured significantly since the first wave of implementations.

Most organizations no longer evaluate solutions based solely on their ability to generate an XBRL filing.

Instead, they focus on capabilities that reduce risk and improve long-term reporting efficiency.

|

Automatic Taxonomy Updates |

Built-In Validation Against Current FERC Rules |

Multi-Form Reporting Support |

Complete Audit Trail And Version Control |

Direct eForms Portal Connectivity |

The Next Phase of FERC Reporting Is Already Underway

The industry has largely completed the transition from traditional filings to structured data reporting.

The next phase is about scale.

As regulators continue expanding the use of structured data and initiatives such as XBRL-CSV gain momentum, reporting teams will be expected to manage larger data volumes with greater accuracy and shorter turnaround times.

This is where the role of FERC XBRL reporting software becomes increasingly strategic.

The objective is no longer simply producing compliant filings. It is creating a reporting environment capable of adapting to future regulatory requirements without increasing operational complexity.

Conclusion

As FERC reporting requirements continue to evolve, finance teams need more than a filing tool. They need a platform that simplifies taxonomy management, automates validation, maintains complete audit trails, and supports accurate submissions across every reporting cycle.

IRIS CARBON® helps energy companies streamline regulatory reporting with purpose-built FERC XBRL reporting software designed for accuracy, efficiency, and compliance at scale.