The 2021 ESEF Filings was the first year for issuers to file their AFRs in the xHTML format with the XBRL markup in accordance with the ESEF economy. The first year of ESEF filing was far from smooth. Issuers faced critical challenges like lack of expertise, XBRL markup, ESEF Taxonomy, software solutions, and incertitude regarding the ESEF mandate itself.

However, the finance and accounts team, auditors, and software providers leveled up to the challenge and helped issuers meet the ESEF compliance mandate.

Needless to say, this was the first year of ESEF filing, and these teething troubles were inevitable and expected.

However, amongst all these challenges the biggest and the most critical one remained ignored. The quality of financial statements is an essential component of a successful ESEF filing, and many issuers overlook this aspect.

Financial statements underwent drastic changes last year, and some of the common issues encountered due to their poor quality were inconsistent duplicates and calculation inconsistencies. These issues affected the accuracy of the financial statements and resulted in unsuccessful ESEF filings.

Appreciating the biggest challenge ESEF filers faced last year which was quality, IRIS Business conducted a quality analysis study. Our study commenced in 2020 and scrutinized ESEF filings over a while.

The findings of our study provide insightful details regarding ESEF filing and are helpful for issuers, software providers, and auditors.

Some of our findings shed light on components like Extension Taxonomy Guidelines, Technical Errors, Calculation inconsistencies, Label Guidelines, Taxonomy packages, Extension guidelines, Anchoring guidelines, etc.

Though the 2022 filings may appear challenging on account of text block tagging, last year learnings and experiences can guide and help in course correction.

Let us look at a few potential challenges that issuers might face for AR 2022 and discuss how to cope with them before the live filing season or active collaboration with the “ESEF flock” (i.e., auditors, Regulators, Software providers, Designers) begins.

Things to Watch Out For in

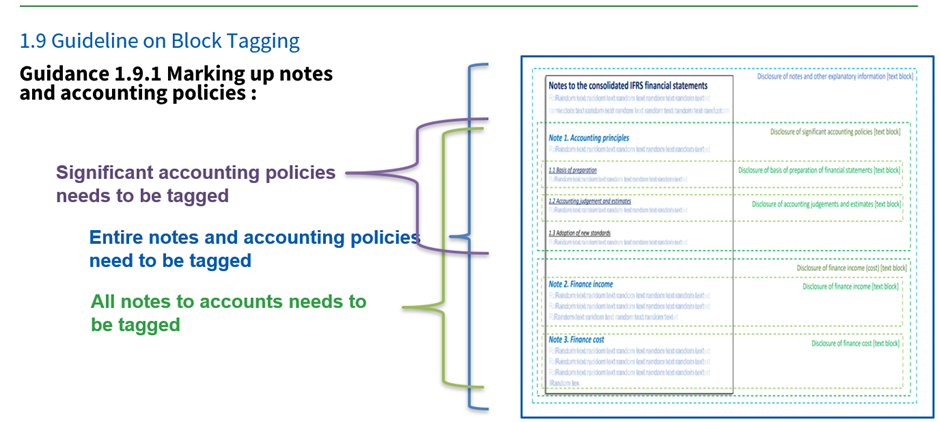

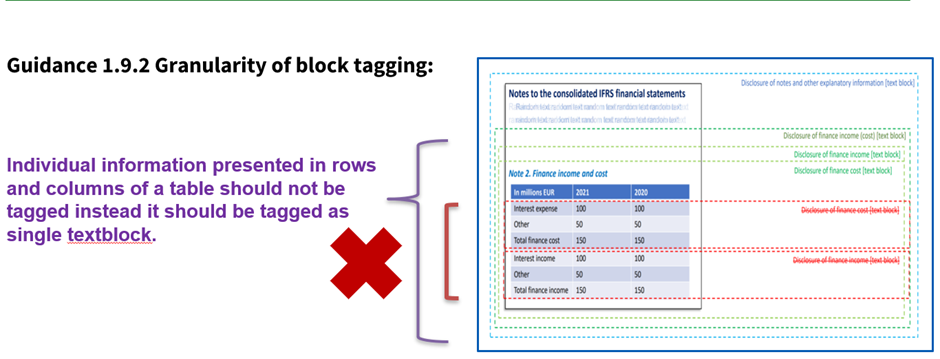

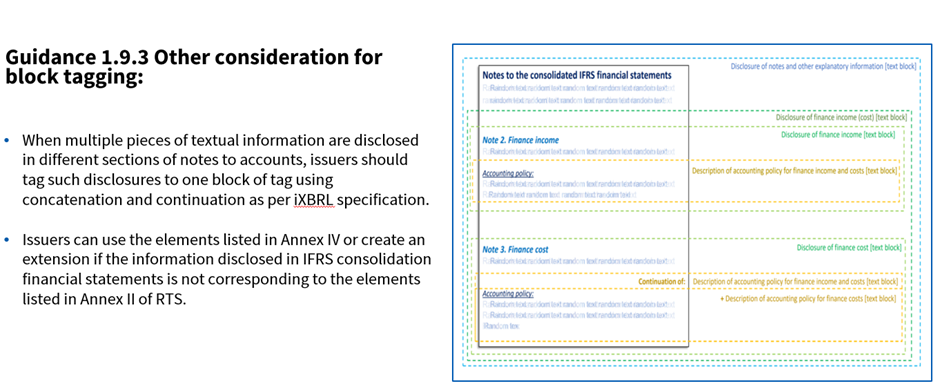

1. Block Tagging

Phase II mandate – Introduction, Mandate & Guidelines

Block tagging is the latest requirement from the European Securities and Markets Authority (ESMA), stating that annual reports produced during the fiscal years on or after January 1st, 2022 will need to have the notes and accounting policies in the financial statements marked up section by section.

Scope

Every Note within the annual financial statements will be tagged as a block of text with XBRL tags embedded in it. Users will be able to view the tags once they click on the notes within the annual financial statements

Tagging Obligation for Parent Company

As per the latest ESEF reporting manual, there is no tagging obligation for a parent company’s Primary Financial Statements. However, local laws and standards govern the regulatory mandate, and few countries like Croatia (regulatory body HANFA) obligate tagging.

Wherever there is no such obligation to tag the Primary Financial Statements, issuers are required to prepare and submit their report in XHTML format. In such cases, issuers must check with their regulator for iXBRL or XHTML requirements for the parent companies.

2. Declaration of Official Language

As per the latest ESEF reporting manual, there is a new requirement that if the companies are filing their AFRs in multiple languages then the companies need to declare or disclose one of the languages as the official language and another language as non-official and mark it as translation. Therefore, before publishing the AFRs (whether in PDF or ESEF format) in two languages, issuers need to ensure that one of the languages is declared as the official language on their website.

3. Latest 2022 ESEF Taxonomy Release and Conformance Suite

The draft RTS (Regulatory Technical Specification) contained that the final report will follow the publication of the 2022 IFRS Taxonomy. The ESEF taxonomy will be updated to reflect the latest available version of the IFRS Taxonomy.

ESMA has submitted this Final Report to the European Commission (EC)and the latter has a period of three months to adopt the regulatory technical standards. Once the Commission adopts and notifies the European Parliament and the Council, they each have a right to object to those standards within a period of three months. This period may further be extended by another three months either by the European Parliament or the Council.

This amendment to the RTS on ESEF is mandatorily applicable for financial years beginning on or after 1 January 2023 and will provide a breather to the preparers. Early application though is allowed.

Therefore, for annual financial reports including financial statements beginning on or after 1 January 2022, issuers will be allowed to use either the 2021 ESEF taxonomy or the 2022 ESEF taxonomy introduced by the draft RTS.

4. Use of Extensions on Studying the Available ESEF Elements

According to the IRIS study on quality analysis, the average extension rate is 15% for all the ESEF filers across Europe. Based on the extension rate, it is recommended to minimize the extension by selecting the broader or narrower ESEF element from the latest taxonomy.

5. Important Considerations for Your ESEF 2022 Filings

- Annual reports in PDF format should be searchable without any images for the portion which needs to be tagged.

- The size of xHTML should not exceed specified MBs. Also, there is a limitation on the size of the (iXBRL) .zip package which needs to be checked with the country-wise regulator before the filings.

- The naming convention used for consolidated and standalone HTML/xHTML documents should be as per ESEF Guidelines which match {base}-{date}-{lang}.xhtml or {base}-{date}-{lang}.html, {base}-{date}-{lang}.zip or as required by the Regulators.

- Validations: The validations for the Text Block tagging will be in accordance with the latest conformance suite release. Currently, there are no updates for the same. Software service providers and auditors are waiting for the latest conformance suit to implement with their solutions. As soon as the latest conformance suit guidelines get released, issuers should make sure that their 2022 iXBRL files are validated and test filed (if available) beforehand.

Conclusion

To conclude, this year is a year of change with the introduction of Block Tagging and issuers will have to plan the AR 2022 ESEF Filing accordingly. In addition to closely following ESMA mandates, they should also actively look out for any specific mandates issued by the regulating bodies of their respective countries for a seamless ESEF filing.

It is also advisable to have a closer look at the quality of the ESEF documents and not ignore the early testing and validation to eliminate last-minute surprises.